Tibi or not Tibi ?

Philippe Tibi was in Dublin last week. France's model for channelling institutional capital into tech funds is going European — and Ireland, with €1–2bn in untapped pension money, has a decision to make.

A year ago, we described the mechanics of the Tibi initiative, the scheme conceived in 2019 by economist Philippe Tibi to channel French institutional savings into venture capital and growth funds. His visit to Dublin last week is a good reason to revisit that story. Since we last covered it, Tibi has comfortably exceeded its targets, and is now positioning itself as the template for a pan-European investment platform. The question being put to countries across the continent, including Ireland, is whether they want to be part of it.

A model that outperformed every forecast

When Tibi submitted his report to the French government in July 2019, the diagnosis was stark: France was producing strong startups but losing them at scale-up stage, either to foreign acquirers or to non-European investors stepping in where domestic capital fell short. His prescription was not another public fund, but a voluntary charter , the "Tibi Charter", inviting insurers and pension funds to allocate a share of their portfolios to approved, labelled VC and growth funds. No government subsidy, near-zero budgetary cost, and a governance structure built around technical committees that vet fund applications.

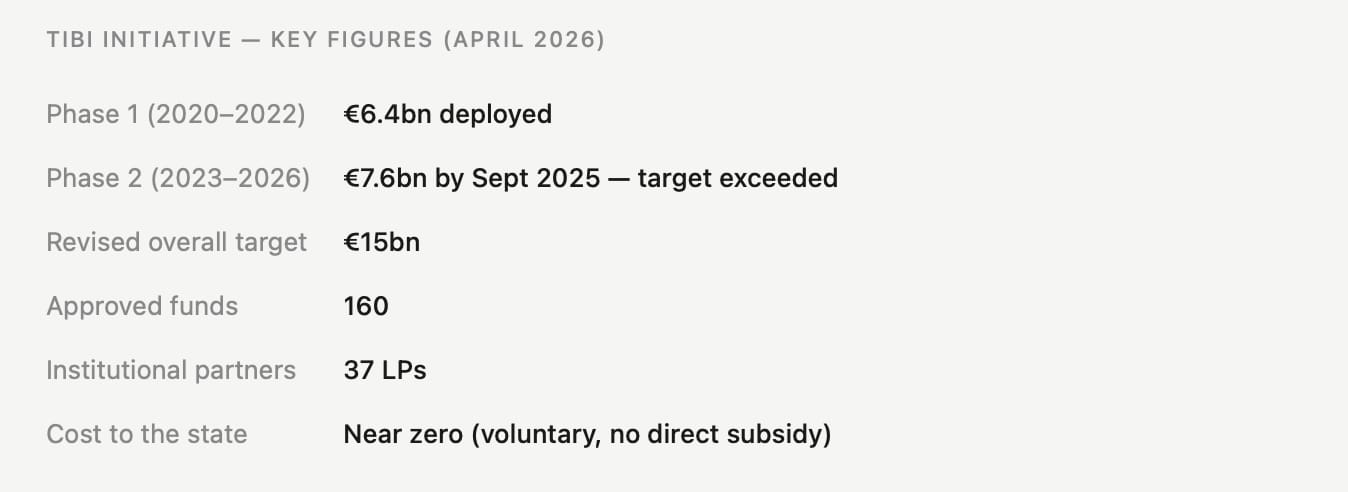

The results have been striking. Phase 1 (2020–2022) mobilised €6.4 billion, exceeding its €6 billion target. Phase 2, launched in June 2023 with a €7 billion goal, had already deployed €7.6 billion by September 2025, more than a year ahead of schedule. The overall initiative target has since been raised from €13 billion to €15 billion. Today, 160 funds carry the Tibi label, 37 institutional investors, including AXA, Crédit Agricole Assurances, Groupama and MAIF have signed the charter, and France has become the leading EU ecosystem for tech investment.

January 2026: the European turn

On 19 January 2026, the French and German finance ministers presented the Noyer-Kukies report, named after Christian Noyer, former governor of the Banque de France, and Jörg Kukies, former German finance minister. Their brief, commissioned jointly in July 2025 under the FIVE initiative (Financing Innovative Ventures in Europe), was to identify concrete measures to close Europe's scale-up financing gap.

"Initiatives like Tibi in France and WIN in Germany should be deployed across all Member States, alongside a similar platform at European level."

— Noyer-Kukies report, January 2026

The report's first and most structural recommendation is to create a European venture capital platform modelled on Tibi and its German counterpart WIN — open to all willing Member States. The idea is to connect national schemes and direct their combined capital toward pan-European VC and growth funds, reducing the continent's dependence on US and Asian investors for late-stage financing. A strengthened version of the European Tech Champions Initiative (ETCI 2.0), managed by the European Investment Fund, would sit at the centre of this architecture.

The report frames this as urgent. In the United States, pension funds account for roughly 50% of private equity and venture capital investments. In Europe, the equivalent figure remains minimal, not for lack of savings, but for lack of a coherent framework to channel them. Tibi and FIVE are attempts to build that framework, one national charter at a time.

Why Dublin?

Philippe Tibi has been running a quiet European roadshow for several years, meeting insurers, pension managers, and startup ecosystem players in Warsaw, Athens, Munich and elsewhere. His presence in Dublin last week fits the same pattern, and the Irish context makes it particularly pointed.

Ireland presents an unusual paradox. It hosts one of Europe's densest concentrations of tech activity, with a deep pool of engineering talent, strong university spinout pipelines, and a startup ecosystem that punches well above its population weight. Yet 75% of venture capital investment in Irish companies comes from international sources, a figure that has climbed from 49% four years ago. That dependence on foreign capital, mostly American, became a visible vulnerability in 2025 as geopolitical headwinds and US policy shifts unsettled cross-border investment flows.

The Irish Venture Capital Association has drawn the connection explicitly. In its pre-budget submission of September 2025, the IVCA cited the Tibi initiative as a benchmark, estimating that a similar Irish scheme could unlock between €1 billion and €2 billion in institutional capital currently sitting in pension funds, insurers and banks, uncommitted to the domestic tech ecosystem. The NTMA, Irish Life, and Zurich Ireland would be natural counterparts to the French signatories of the Tibi Charter.

The mechanics translate well. The Tibi model requires no new public fund and no direct subsidy. What it requires is a coordinating institution willing to run technical committees, vet fund applications, and maintain the label, a role that Enterprise Ireland or the Department of Finance could plausibly play, mirroring what the Direction du Trésor does in France.

What this means for Franco-Irish actors

The convergence between Tibi's European expansion and a potential Irish equivalent opens concrete possibilities. Funds already operating across both ecosystems, Atlantic Bridge Capital, which has offices in Dublin, Paris and London, is the clearest example, are precisely the kind of cross-border growth vehicles that a European platform would be designed to channel. A Tibi-style label at European level would make it easier for Irish institutional LPs to invest in funds with Franco-Irish mandates without each needing to build separate due-diligence processes from scratch.

For scale-up companies on both sides, a better-capitalised European investment landscape means more funds capable of writing Series B and C cheques without defaulting to New York or San Francisco. It also means less pressure to relocate or accept early acquisition by non-European strategics, a dynamic that has consistently drained promising companies out of both the French and Irish ecosystems.

And for Irish institutional investors themselves, the French experience offers something arguably more useful than a blueprint: proof that this class of asset allocation is compatible with fiduciary obligations, provided the framework is rigorous, transparent, and well-governed. Seven years of Tibi data, across two full phases, through a rate-hiking cycle and a global tech correction, give them something to underwrite against.

So, Tibi or not Tibi?

A third phase of the initiative is expected later in 2026, with European ambition as its defining feature. The French and German finance ministries have listed the launch of the pan-European platform as their "first operational priority" in their joint January roadmap. Other Member States are already in informal discussions.

Philippe Tibi's visit to Dublin suggests Ireland is part of that conversation. The conditions are there: a proven model, a clear financing gap, and institutional investors who have the capital. The IVCA has already made the case. What comes next is an opportunity — for the ecosystem, for institutional actors, and for policymakers — to shape how European tech investment is structured from the inside.

As Hamlet nearly said: that is the question.